Star Alliance are launching a common currency credit card, with Australia earmarked as the launch market. The premise of the card being that points earned on the card could be transferred to and redeemed on any of the 26 Star Alliance member airlines.

Depending on the response it receives in Australia Star Alliance may take the card to other markets too, although there is no timeline for doing that at this stage.

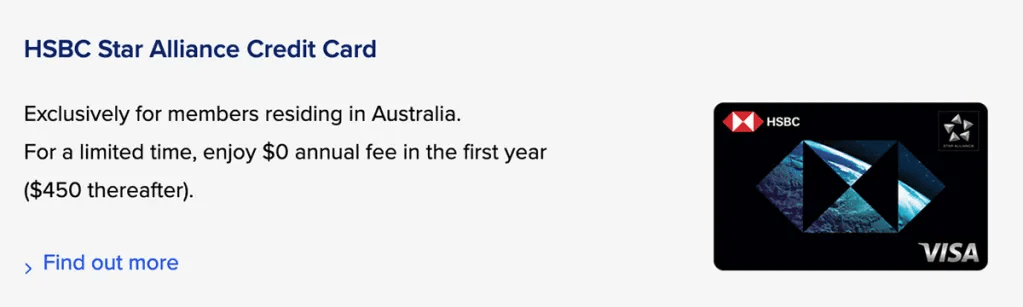

HSBC Star Alliance Card

Applications for the card are not open yet and we don’t know the date that will happen. It is likely though that you will be able to apply for the card before the year is out.

We knew a proposal like this was in the offing, in-fact I had recently alluded to it over here. A lot of the minor details seem to be missing at the moment, but based on the information provided by one of major alliance member Singapore Airlines, this is what we know:

HSBC Star Alliance Card

- The card will be marketed through HSBC in Australia and use VISA’s payment network to process transactions.

- It will carry an annual fee of $450, which will be waived in the 1st year for early bird applicants. As the applications for the card aren’t open yet, we don’t know how long the $0 annual fee offer will last.

- The card’s common currency will be known as Star Alliance Point.

- Cardmembers will earn 1 Star Alliance Point per $1 of eligible spend on up to $3,000 per month, then 0.5 Star Alliance Point per $1 thereafter.

- It is understood that cardmembers will be able to nominate any 1 of the 26 Star Alliance member airline as their Status airline. The Star Alliance Points earned on the card will be converted and transferred to the Frequent Flyer Account of the nominated airline automatically each month.

- Cardmembers who nominate Singapore Airline as their Status Airline will be able to earn KrisFlyer Elite Gold status for 12 months by spending $4,000 within 90 days of card approval. To retain the status beyond 12 months, they will need to spend at least $60,000 on the card in each 12-month period.

Singapore Airline is a member of Star Alliance

PointsHq is on Instagram – PointsHq 👈🏽

What I like about the card

My initial impression is that just like most things in life, the card is a bit of a mixed-bag. Let’s take a look at the positive aspects of the card.

Choice of HSBC & VISA

I like the fact that Star Alliance have chosen HSBC to market the card. At first this might seem like a curious choice, but when you think about the home markets of the 26 member airlines, markets where members are most likely to pick up the card, I can’t think of another bank with a similar reach or brand recognition.

Citibank could have made the cut, but it’s dwindling retail footprint outside of the United States would have ruled it out.

The choice of Visa is unsurprising too, alongside Mastercard it’s cards are the most accepted globally. With low (but improving) acceptance and comparatively high merchant fee, I doubt American Express would have been in the running.

Common Currency

Why didn’t anybody think about this earlier? There is so much to love about the fact that Star Alliance loyalists living anywhere can benefit from it. Let me explain.

Imagine an Avianca LifeMiles Frequent Flyer based in Colombia wanting to redeem miles for Singapore Airlines Business or First Class flights. In theory, miles from any Star Alliance carrier should be redeemable on other member airlines, in practice however, we know that some carriers such as Singapore Airlines do not release premium cabin award space to partner airlines.

With a Star Alliance credit card, (assuming that it is made available in Colombia), this member can choose to funnel Star Alliance Points to their KrisFlyer account instead and overcome this barrier.

If your home country counts a Star Alliance member as a home carrier, chances are there will be other cards offering you the opportunity to earn points and miles into the carriers Frequent Flyer Program. In those instances, it might make a lot more sense to direct the earnings from your Star Alliance card to a carrier whose miles are harder to earn or someone who restricts award space to members of partner airlines.

Elite Status

We don’t yet know whether other member airlines will follow the footsteps of Singapore Airlines and let members earn status merely by putting a certain amount of spend on that card. If they do, this will be of great benefit to the occasional, Economy class flyer.

Top tier status in any Star Alliance carrier maps to Star Alliance Gold, meaning you can take advantage of the elite status no matter which airline you fly. Some of the most valuable benefits of Star Alliance Gold status are:

- Priority Check-in and Boarding.

- Complimentary lounge access for the member and a guest at more than 1,000 lounges worldwide.

- Increased checked baggage allowance.

- Free Upgrade to Business First Class on the Heathrow Express trains.

Access to lucrative Frequent Flyer Programs

Although the Star Alliance is a collection of 26 equal member airlines, their Frequent Flyer Programs can hardly be more unequal. For instance, Air New Zealand’s Airpoint program is routinely ridiculed as one of the worst (if not the worst) program in the world.

On the other hand, there are Frequent Flyer Programs such as Air Canada’s Aeroplan, ANA’s ANA Mileage Club and Avianca’s LifeMiles that offer incredible value. Although comparing the value of individual programs is outside the scope of this post, let me give you a quick example.

- A one-way Business Class Seat flying Singapore Airlines between Sydney and Tokyo will set you back 100,500 KrisFlyer Miles.

- You can fly ANA Business Class between Sydney and Tokyo return for as few as 65,000 ANA Miles.

ANA B-787 Business Class Cabin

Until now, it has been very difficult to earn points in programs such as ANA Mileage Club or Aeroplan. The HSBC Star Alliance card will solve that problem for savvy points and miles collectors.

What I do not like about the card

The HSBC Star Alliance card is not without its shortcomings, which in some instances may be enough to dissuade some people from getting it. Let’s take a look at few of them.

Low Earnings & Transfer Rate

The card earns 1 Star Alliance Point per $1 on all purchases. There are no category bonuses that we sometimes see with other cards. For instance, Westpac Black Altitude card earns up to 6 Altitude Rewards Points per $1 on spending with about a dozen odd partners including Singapore Airlines and Emirates. At the transfer rate of 3:1, this is like earning 2 KrisFlyer Miles or 2 Emirates Skywards Miles per $1 in spend.

If that isn’t mediocre enough, the earning rate is drastically slashed to just 0.5 Star Alliance Point per $1 on spends above $3,000 in a month.

Similarly, the conversion ratio from Star Alliance Points to KrisFlyer Miles is abysmal at just 1:0.8 (1 Star Alliance Point = 0.8 KrisFlyer Mile). We don’t yet know what the conversion rates will be to other member programs, but anything less than 1:1 is sure to put off a fair few members from taking up the card.

Fixed Transfer Partners

What is the point in having a transferrable currency if you are going to restrict the transfer to a single partner? To my mind, this is the card’s single biggest stumbling block. Let me explain.

As I mentioned earlier, when you apply for the HSBC Star Alliance Card, you will be required to nominate a Status Airline. Then at the end of each monthly statement cycle, all the points you have earned in that month will be automatically swept into the account of your nominated airline. If this was Singapore Airlines, points will be deposited into your KrisFlyer account. This massively kills the value proposition.

One of the reasons American Express Membership Rewards Points is so highly valued is because of the flexibility it offers. You can hold your points with Amex as a single unit for as long as you want, and in the process also take advantage of various transfer bonuses along the way. When you are ready to fly and have found confirmed award space, you manually transfer the points to the partner of your choice.

This approach doesn’t simply make Membership Rewards Points more versatile, but also helps protect their value in case one of the transfer partners decide to devalue their program. Now it could well be that cardholders receive an option to switch their Status Airline every so often, in my view though, that isn’t nearly as attractive as the ability to freely transfer points.

High Spend threshold to earn elite status

We don’t know if, or which other airlines will allow members to earn elite status based on spending, if they do, what will be that threshold? So I make this point solely on the basis of what we know in relation to Singapore Airlines.

A $60,000 per year (average $5,000 per month) spend on a ‘mid-market card‘ is too high to justify when you consider the opportunity cost of doing it. And while some people might be able to benefit from this, the fact is that vast majority of points and miles collectors aren’t saving points to fly Economy. A Business Class ticket offers many of the perks and benefits that come with elite status anyways, which in my opinion limits the value of this benefit.

Lack of Welcome Bonus

Australian’s are lucky to live in an extremely rewarding ecosystem of points and miles. It isn’t quite as lucrative as the United States, but there is no shortage of cards offering sign-up bonuses of 100,000 points or more.

In that context, it is surprising that the HSBC Star Alliance Card is not offering a Welcome Bonus. Yes the annual fee will be waived in the first year for early adopters of the card and that is great, but as a new entrant in a highly competitive market, I would have expected some sort of Welcome Bonus thrown in the mix.

In Conclusion

Star Alliance credit card is coming to Australia. The card isn’t currently taking applications, but is expected to do so very soon. On one hand it excites you with the prospect of access to many Frequent Flyer Programs not hitherto available in Australia, on the other, it underwhelms you with the lack of welcome bonus and some lukewarm earning and transfer rates.

It is also frustrating that points from the card are tied to a single frequent flyer currency at any given time and there is no ability to make the transfers manually. Considering everything that we know, plus a whole lot of unknowns, the only sensible thing to do for now will be to reserve making a value judgement on the card.

I plan to write more on the card particularly as new information becomes available. I will also be talking about the sweet-spots that lie buried in several of the partner programs.

Based on what you know, are you likely to apply for the card? Leave a comment below.

PointsHq is on Instagram – PointsHq 👈🏽

Comments